DOES NOT INCLUDE TECHNICAL CORRECTIONS RELIEF FOR THE “DOWNWARD ATTRIBUTION” PROBLEM CREATED BY THE 2017 TCJA

The House passed legislation on Tuesday, December 17 that is expected to pass the Senate and be signed by the President. It mainly focused on tax extenders (some that had expired as far back as the end of 2017) but did nothing to help US Shareholders of foreign entities that have been sucked into the Controlled Foreign Corporation (CFC) regime even though these CFCs are not really controlled by US Shareholders.

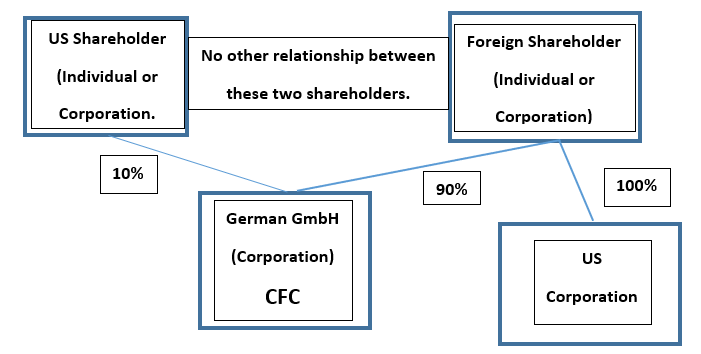

For example, a US Shareholder who owns 10% of a CFC picks up income earned by the CFC that has not been distributed merely because it falls under the so-called GILTI (Global Intangible Low-Taxed Income-Sec. 951A) provision. This “tainted” income for US tax purposes is often normal operating income (not really passive dividend and interest income) earned in a foreign entity that is paying tax at a rate similar or even higher than the US tax rate (e.g., Germany).

The international tax community was hoping this correction would be passed as part of year-end legislation and relieve certain US Shareholders from this deemed taxable income issue where there is no cash distribution to pay the tax and the minority US Shareholder has little control over the activities of the foreign entity.

At least there was one good international tax extender provision passed under the legislation related to the so called “look-through” provision, extending the benefit for 2020. This merely avoided (in most cases) a situation where dividends or interest paid from one CFC to another CFC – and not actually distribution to a US Shareholder – would be considered “tainted” income (i.e., Subpart F income) and deemed distributed as taxable income to the US Shareholder. Like other extender provisions, this has been around for a number of years (since 2006) but has never been made permanent. Instead, Congress goes through this annual exercise of “chicken” every couple of years.

It is hoped that eventually this downward attribution error will be corrected in the future, which now is unlikely until after the next election. In the meantime, US Shareholders in the situation below must suffer taxation that was not intended.